Why's picking life insurance such a major financial crossroad? You'll understand that protection's necessary, but technical terms'll often make the choice feel difficult. Two options'll appear most often, and they're term insurance and whole life insurance.

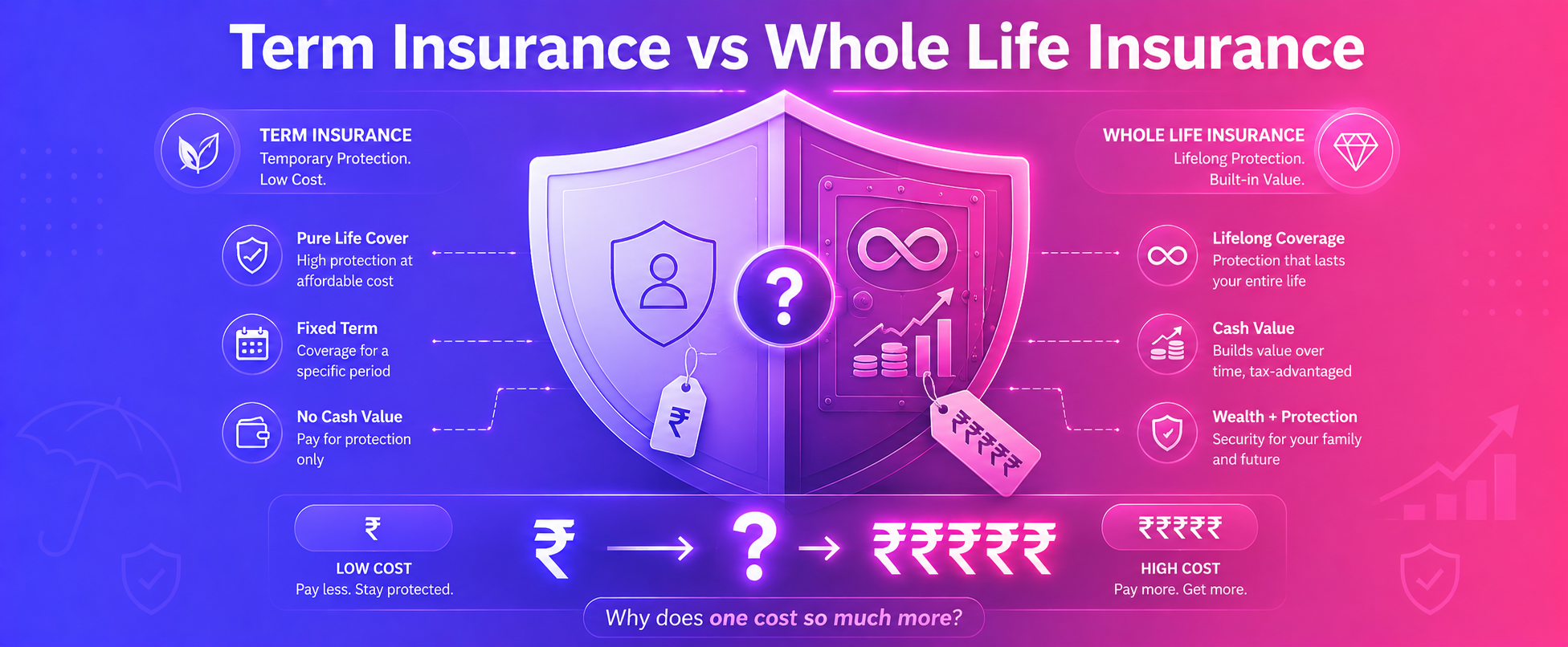

Term insurance's simple. It'll offer temporary, cheap protection for a set timeframe. Families'll often use it to cover mortgage debts or the years when kids live home. In contrast, whole life insurance's a permanent plan. It'll combine lifelong coverage with a savings part, which's sometimes called cash value. Since it'll impact your budget and flexibility, the difference between term and whole life insurance's worth understanding.

By following this guide, you'll see the difference between term and whole life insurance clearly. Later on, you'll pick a plan that doesn't ignore your budget or your goals for the future.

Key takeaways

It's worth checking these main points before you're in the details.

- For many, [term insurance]'s the pick for high payouts at low prices to cover mortgages.

- Under whole life plans, costs are higher. Still, coverage never expires and builds cash value.

- You don't get a payout if you outlive the contract.

- While term plans provide basic safety, whole life's better for legacy planning.

What is term life insurance?

Term life insurance is a temporary shield. Since it isn't permanent, you'll lose coverage once the term expires. Only when you pass away while the policy's active does your family receive a payout.

- If you die within a 10, 20, or 30 year window, your beneficiary receives a death benefit.

- You don't get cash value here because these plans focus on pure protection, not investing.

- Many parents use this to replace income while paying off a mortgage or raising children.

What is whole life insurance?

Whole life insurance isn't a temporary plan. It's active forever as long as you pay the premiums. While some policies end after a set term, this one lasts until you reach age 100.

- This policy pairs a set payout for families with a cash value account that works like savings.

- Borrowing money or taking withdrawals is possible because the government doesn't tax the growth yet.

- Families get a reliable safety net that helps them handle estate taxes.

Term life vs whole life insurance: a side-by-side comparison

You might find it helpful to see how these options vary.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| How long it lasts | A set time like 10 or 30 years | Your whole life, often up to age 100 |

| What you pay | Usually lower, especially if you are young | Higher, and sometimes by a large amount |

| Cash value | Cash typically doesn't grow here | It often builds up over time with tax perks |

| Payout style | Most only pay if you die during the term | Gives a death benefit plus cash savings |

| Main purpose | Replacing income or short debts | Long term legacy planning or permanent savings |

Key advantages and disadvantages of each policy

Each policy type's defined by its own set of pros and cons. Decisions'll usually depend on your specific financial goals. Your situation's what dictates which path makes sense.

What makes term life insurance worth considering

Selecting term insurance'll offer several advantages for modern households.

- Affordable premiums aren't the only draw, but they're the biggest. For a much lower cost than whole life insurance, you can secure a large death benefit.

- The structure's easy to understand. You keep up with payments for a set period, and the insurer pays out if you pass away during that time.

- Young parents'll often choose a twenty year policy to align with a mortgage or the time it takes for children to finish school.

Are you starting a career? This option'll usually work for tight budgets. It'll provide a large safety net without a massive bill.

Where term life insurance falls short

No plan's perfect. Keep these specific limitations in mind before you sign any paperwork.

- There's no investment component here. Your money pays for protection only, meaning you won't build up any equity to use later.

- Protection's just a temporary fix. When the term ends, the policy disappears, which could leave you without a safety net in your old age.

- Buying a new policy later in life is pricey. Rates'll jump up as you age or if your health changes.

Once that clock's stopped, the protection vanishes. Then you'll either buy a more expensive plan or go without.

What whole life insurance gets right

Whole life policies'll provide a sense of permanence that changes how they fit into a financial plan.

- This coverage'll last for your entire life. So long as you pay the premium, the policy stays active.

- Part of your payment goes into a cash value account. This fund'll grow over the years, and you can take loans against it if needed.

- Your family'll receive a payout eventually. That makes it a solid choice for those focused on leaving an inheritance.

If you've got the extra cash, these plans function as a long term asset. Determine how much extra you can afford to pay each month.

The downsides of whole life insurance

Choosing permanent protection'll require some trade offs that are worth thinking about.

- The monthly bill's much higher. You might pay five or ten times more than you'd pay for a term policy with the same death benefit.

- Managing these products isn't simple. Dealing with dividend rules or policy loans'll be quite a headache for most people.

- Cash value growth'll usually feel slow. Often, the returns don't match what you'd get by putting that money into a brokerage account.

Expect to pay these high premiums for decades. If you stop, you'll lose the benefits.

How to find the best term insurance plan for your needs

If you've decided term insurance works, comparing policies comes next. Most people use a fast, data-backed method today because it removes the guesswork.

- Input your age, yearly income, and any outstanding debt into the Cover Tiger portal.

- The tool calculates a recommended coverage amount based on your finances.

- Because the priority is fit instead of sales commissions, you're able to evaluate various premiums and riders across providers.

Digital tools let you bypass biased recommendations to find term insurance. You won't have to worry about picking the wrong policy.

Which policy is right for you: term or whole life insurance?

Deciding on a plan involves more than just a surface level look. Check your debt and age. These factors usually determine the choice that's right for you.

Choose term insurance if...

- Low monthly payments are a priority but your family still needs a large payout.

- Temporary debts, such as tuition or a home loan, do not need coverage forever.

- By spending less on premiums, you gain the freedom to manage personal investments in the stock market.

Choose whole life insurance if...

- High net worth individuals need a reliable way to move wealth to the next generation.

- Permanent protection is required because a family member with special needs will always depend on that money.

- Tax advantaged cash value is an attractive option once you have already maxed out your other retirement savings.

Can you have both?

Combining these two products often provides the best balance for most families. Keeping a small whole life policy ensures money is always available for final expenses or a small inheritance. It will work. At the same time, a larger term policy protects against major financial disasters while children are still growing up. This approach maintains a lifelong base of support while using cheaper term rates to handle the most expensive decades.

Compare term insurance quotes instantly with cover tiger

For most Indian households, term insurance is the most practical way to shield a family's financial future. Rates shift. Since riders vary between providers, you should compare several options before buying.

Cover Tiger makes this easier.

Because the platform suggests plans based on your specific life situation, results don't focus on commission incentives. You'll view benefits and premiums side by side. Get a quote in minutes so you do not wait.

Conclusion

Deciding between these options usually comes down to your budget and long-term goals. Term insurance offers high coverage at a low price for a specific number of years, which helps with income replacement or mortgage protection. Whole life insurance provides a death benefit that never expires and includes a savings component, but you'll pay much higher premiums for those features.

One plan isn't objectively better than the other.

The best fit depends on why you need the money. Term insurance is typically the winner for simple protection. But whole life insurance might work for estate planning or lifelong needs. Look at your debts and your family's future. It is a good idea to use an online tool to compare the costs.

FAQs

1. Which insurance is better, term or whole life?

Choosing between these options usually depends on your financial goals. No single policy works for every individual. For those seeking a large death benefit at a low cost for a set period, term insurance often makes more sense. It is a matter of aligning the coverage with your specific family needs and current budget.

2. Do you get money back at the end of term life insurance?

Standard policies do not pay out a single cent if you happen to outlive the contract length. Once that specific time is up, the insurer keeps the money. "[Return of premium]" add-ons exist to give the cash back, but they cost noticeably more than basic plans. Most people find the extra cost isn't worth the refund when they look at their monthly budget. It is like paying extra for a savings account that yields nothing.

3. Can I convert term life to whole life?

Many policies have a conversion clause that allows a switch to permanent coverage without a new medical exam. This is a helpful way to keep protection active as your health changes over time. There is usually a specific time window for this change before the option disappears forever. You should look at your contract for the exact age limit so the opportunity isn't lost.

4. Can you cash out whole life insurance?

Whole life builds a cash value component that you can access later. You might take a loan or make a direct withdrawal, though there are risks involved. If a loan remains unpaid, your beneficiaries receive a smaller payout. Tax implications could also apply if the amount taken exceeds what you paid in premiums. Keep in mind that this money belongs to the policy owner, not the heirs. Borrowing against the value can be useful for emergencies, but it reduces the death benefit if you don't pay it back.

5. What happens to a 20 year term life insurance policy after 20 years?

Once that twenty year period ends, the coverage effectively vanishes. The policy terminates and no payout occurs because you outlived the term. This can be a shock if you still have financial obligations. If you still require life insurance, you could try to renew the existing policy, but the new rate will likely be much higher. Another option is to convert the plan to permanent insurance or apply for a fresh policy based on your current health status.

6. Are the premiums for whole life insurance fixed for life?

Premiums for traditional whole life plans generally stay level for your entire life. The amount you pay at age thirty is the same amount you will pay at age eighty. This provides a predictable way to manage a long term household budget. Still, it is smart to read the fine print to ensure the contract lacks triggers that could increase costs.

7. Which policy is generally recommended for covering a home loan?

For protecting a mortgage, term insurance is the standard choice because it is affordable and straightforward. It provides enough funds for your family to pay off the house if you pass away during the years of the loan. This is a very smart way to handle a big debt without spending too much on premiums. It ensures your family stays in their home. You won't have to worry about the bank taking the property if the primary breadwinner is suddenly gone.

8. Can I have both a term and a whole life insurance policy at the same time?

Maintaining both types of coverage is a common strategy for many households. You might hold a small whole life policy for funeral costs while using a large term policy to protect your children until they reach adulthood. This layering method offers a balance of permanent and temporary protection. This strategy allows you to cover shifting liabilities like a mortgage or tuition without a lifetime commitment to high premiums.